Prefer it or not, firms are judged

by flawed requirements.

GAAP generally misrepresents enterprise actuality. Let’s use that reality to generate some alpha.

Persevering with from the first memo, we’ll begin by inspecting income recognition, the money conversion cycle, and free money circulate.

“Income” isn’t income, it’s contract timing.

Income is acknowledged when a contract

between a enterprise and a buyer has been carried out.

Right here’s the way it’s carried out in response to FASB:

The Income Recognition Course of

1. Determine the contract with a buyer.

2. Determine the efficiency obligations (guarantees) within the contract.

3. Decide the transaction value.

4. Allocate the transaction value to the efficiency obligations within the contract.

5. Acknowledge income when (or as) the reporting group satisfies a efficiency obligation.

Supply: FASB

There are a number of areas the place GAAP

income recognition can hit a snag and you will discover a possibility.

1. Multiparty Transactions

In multiparty transactions, “income” can imply gross income {dollars} in a transaction or a subset that’s acknowledged as one firm’s internet income. Your final $20 Uber journey most likely generated $16 in internet income for the driving force and $4 in internet income for Uber.

Internet income can get distorted when a number of events transact earlier than an finish buyer receives a product. Think about {that a} drug producer controls a distributor and the distributor will increase its orders in anticipation of finish buyer demand. These new orders puff up the producer’s internet income numbers. However what if the tip buyer demand doesn’t materialize? The producer’s reported natural income development would possibly simply be pulling ahead future income and stuffing it into the distribution channel. These class definition video games can current traps for development traders and potential alpha for shorts.

2. Adjustments in Efficiency Standards

When efficiency standards change, reported income can develop into an unstable metric. For instance, the identical software program sale may end up in totally different GAAP income numbers relying on whether or not it’s structured as a license or a subscription. Subscriptions present much less GAAP income early on however might cut back buyer churn over time. Shrinking GAAP income isn’t a very good look within the public markets. That’s why the perpetual-license-to-SaaS transition is a well-liked personal fairness play: You’ll be able to take an organization personal to alter its accounting customary outdoors of the highlight, then deliver the corporate public with freshly cleaned books and a brand new story. Corporations that do make this sort of transition whereas public, like Adobe, can current significant alpha alternatives for traders who perceive how the long run accounting will end up.

3. Multiyear Contracts

Ought to it matter if a transaction is acknowledged on 31 December or 1 January?

Corporations need to report robust year-over-year development for every interval. Savvy clients wait till the tip of 1 / 4 after which ask for a reduction to e-book a transaction earlier than the interval ends. It’s much like shopping for a used automotive after Christmas from a salesman who’s determined to make their year-end quota. In dangerous eventualities, an organization can get caught pulling ahead discounted demand each quarter simply to chase final yr’s numbers. Within the worst case, that firm will run out of future demand to tug and their gross sales pipeline will fall flat.

However GAAP doesn’t make it simple to tell apart between quickly pulled ahead contracts (noise) and rising buyer demand (sign). That is additionally true in reverse — GAAP income doesn’t differentiate between slowing buyer demand (sign) and momentary gross sales delays (noise).

Personal traders can have a look at what I’ll name “the contract time period construction.”

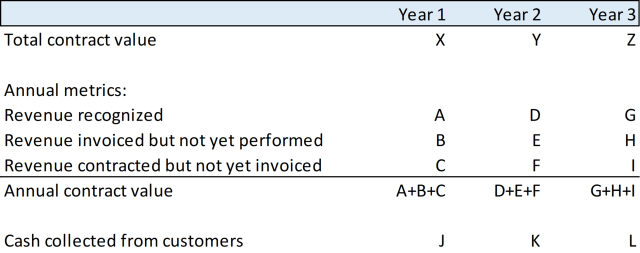

The Contract Time period Construction

What you’d actually prefer to see in GAAP is annual contract worth (ACV) and complete contract worth (TCV). ACV is the quantity of enterprise presently underneath contract for that yr — whether or not it’s already acknowledged as income, invoiced however not carried out, or contracted however not but invoiced. TCV consists of contracts and invoices for future years. With ACV and TCV, you possibly can see income recognition throughout the context of the complete gross sales image.

However any FASB proposal so as to add the contract time period construction to GAAP would meet with stiff resistance. College could be loads simpler in case you might grade your personal homework. Think about a excessive schooler’s incentive to present their dad and mom “robust steering” for this semester’s report card. Even the very best college students would need to maintain their efficiency secret — why let the competitors know the way you’re doing? So the contract time period construction will probably keep hidden and, thus, be a great spot to hunt for alternatives.

Income is simply GAAP contract timing.

As long as public traders chubby these reported numbers, the

contract-to-revenue recognition course of ought to stay a recurring alpha supply.

The money conversion cycle must be measured as a share and embody deferred income.

The money conversion cycle

(CCC) measures how lengthy every greenback of working capital is invested within the

manufacturing and gross sales strategy of a mean transaction.

The concept is to trace working capital

effectivity from the money paid to suppliers to the money collected from clients.

The Money Conversion Cycle (Present Method)

The CCC is sort of a mini return on

fairness (ROE). Every driver will be improved with a view to improve the return on

working capital. However sadly, there are two flaws with the present CCC

metric.

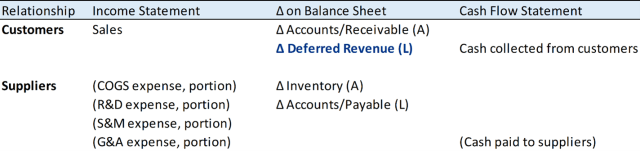

The primary downside is that the CCC is calculated in days. What we’re actually measuring is capital effectivity over a time frame, often a yr. That’s a ratio. No person calculates ratios in days. We should always measure the CCC as a share.

The second and extra essential downside

is {that a} time period is lacking. The CCC presently consists of accounts receivable (money

owed by clients), accounts payable (money owed to suppliers), and stock

(money paid prematurely to suppliers).

What’s lacking is present deferred income (money collected prematurely from clients). It’s simple to see the CCC’s oversight once we have a look at the opposite working capital line gadgets associated to clients and suppliers:

The Money Conversion Cycle Ought to Embrace Deferred Income

Updating the CCC makes it simpler to

determine capital-light companies.

Companies that accumulate money from their clients forward of contract efficiency (deferred income) will be extremely cash-efficient. But when the CCC excludes deferred income, then traders would possibly overlook that these companies can develop at GAAP internet revenue losses with out dilutive fairness raises. This omission might clarify why SaaS and client subscription companies had been misvalued 5 years in the past. If you will discover the parallel in the present day, you’d be like the general public SaaS traders of 2016, nicely forward of the curve.

The up to date CCC additionally makes it simpler to flag the dreaded SaaS loss of life spiral. Shortly rising firms will be fairly fragile after they rely on deferred income to fulfill ongoing money wants. If their GAAP income development peters out, they might quickly discover themselves in a money shortfall. Bizarrely, these firms can present wonderful GAAP income numbers whereas teetering on the sting of chapter. If the CCC doesn’t embody deferred income, you received’t be capable of see the canary within the coal mine.

“Free money circulate” isn’t free money circulate, it’s an accrual metric.

“Free money circulate” doesn’t all the time equal the precise money generated by a enterprise.

This raises an issue for educational finance as a result of the keystone mannequin for inventory valuation is John Burr Williams’ discounted money circulate (DCF) evaluation. You would possibly ask, if traders can’t reliably measure free money circulate (FCF), how can they reliably low cost and worth these money flows? Good query.

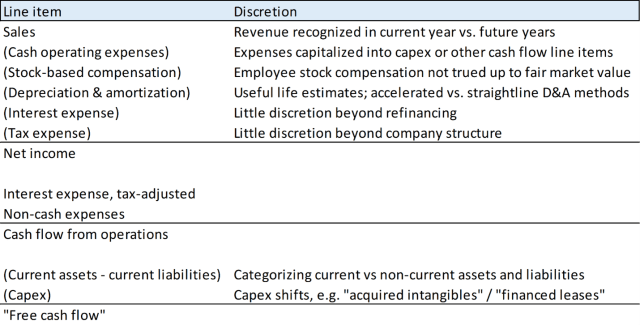

Right here’s the usual definition totally free money circulate:

The Normal Free Money Move Equation

| Issue | Location |

| + Money Move from Working Actions | Assertion of Money Flows |

| + Curiosity Expense | Revenue Assertion |

| – Tax Protect on Curiosity Expense | Revenue Assertion |

| – Capital Expenditures (Capex) | Assertion of Money Flows (Money Move from Investing Actions) |

| = Free Money Move |

Supply: Investopedia

This all appears easy till

you have a look at how a lot discretion goes into the accrual numbers for a given

interval and the way a lot these accrual numbers influence FCF.

Why “Free Money Move” Would possibly Not Be Free Money Move

Internally-developed intangible belongings are the hazard space in in the present day’s market. Most traders agree that we must always capitalize some portion of R&D and SG&A bills, however nobody is certain how lengthy these intangible belongings will final. Google’s search engine ought to endure in some kind for many years to return; AskJeeves, not as probably. How can we give you a constant rule to amortize the Google and AskJeeves engineering efforts ex-ante?

To make issues worse, intangible capex could also be hidden in line gadgets that aren’t included in FCF calculations. Should you look carefully, an organization’s acquired intangibles and financed leases would possibly simply be capex in disguise. Correctly accounting for internally developed intangibles often is the most important unsolved downside in GAAP.

Traders who concentrate on free money circulate yield typically analogize fairness dividends, rightly or wrongly, to bond coupons. However as a result of present FCF is chock full of those accrual assumptions, we will’t naively challenge present FCF to estimate normalized FCF. Corporations have a robust incentive to pump that perceived fairness coupon. That juiced FCF yield is akin to a shaky bond with a excessive yield, often known as a idiot’s yield.

The alpha alternative is figuring out when normalized FCF will differ considerably from present FCF. Shares the place the corporate wants to chop the fairness yield — be it dividends, inventory buybacks, or debt funds — will be good shorts. Lengthy alternatives can come up when a significant portion of present capex, R&D, or gross sales spend flips to an amortizable fastened price. The actual problem is guaranteeing that the fastened asset you’re betting on isn’t about to develop into stranded — lest you find yourself backing AskJeeves as a substitute of Google.

Transferring to the Steadiness Sheet

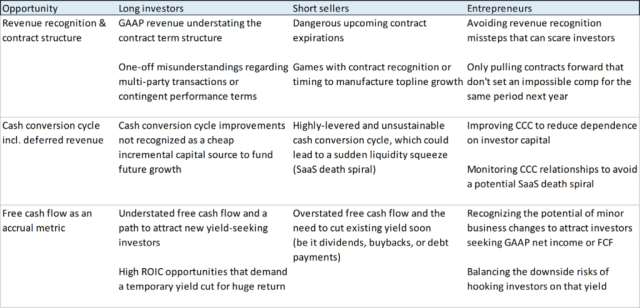

Right here’s how the puzzle items start to suit collectively for longs, shorts, and entrepreneurs:

We will recharacterize the stability sheet too. From there, we will revisit the weighted common price of capital in addition to the market worth of fairness and share-based compensation.

You’ll be able to learn extra from Luke Constable in Lembas Capital’s Library.

Should you favored this publish, don’t overlook to subscribe to the Enterprising Investor.

All posts are the opinion of the creator. As such, they shouldn’t be construed as funding recommendation, nor do the opinions expressed essentially replicate the views of CFA Institute or the creator’s employer.

Picture by Darío Martínez-Batlle on Unsplash

Skilled Studying for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report skilled studying (PL) credit earned, together with content material on Enterprising Investor. Members can file credit simply utilizing their on-line PL tracker.

![]()

Luke Constable

Source link